Japan is known globally as a “frugality superpower.” It is a society where waste is considered a vice and being “smart with money” is a highly respected trait. Before we dive into the specific tools, it’s important to understand the cultural mindset: Japanese saving isn’t about being stingy; it’s about mindfulness. It’s the art of knowing where every yen goes and finding satisfaction in a simple, well-managed life.

But as a resident since 2018, I’ve seen a shift. The legendary “saving myth” that has protected Japanese households for decades is starting to show cracks under the pressure of a new economic reality.

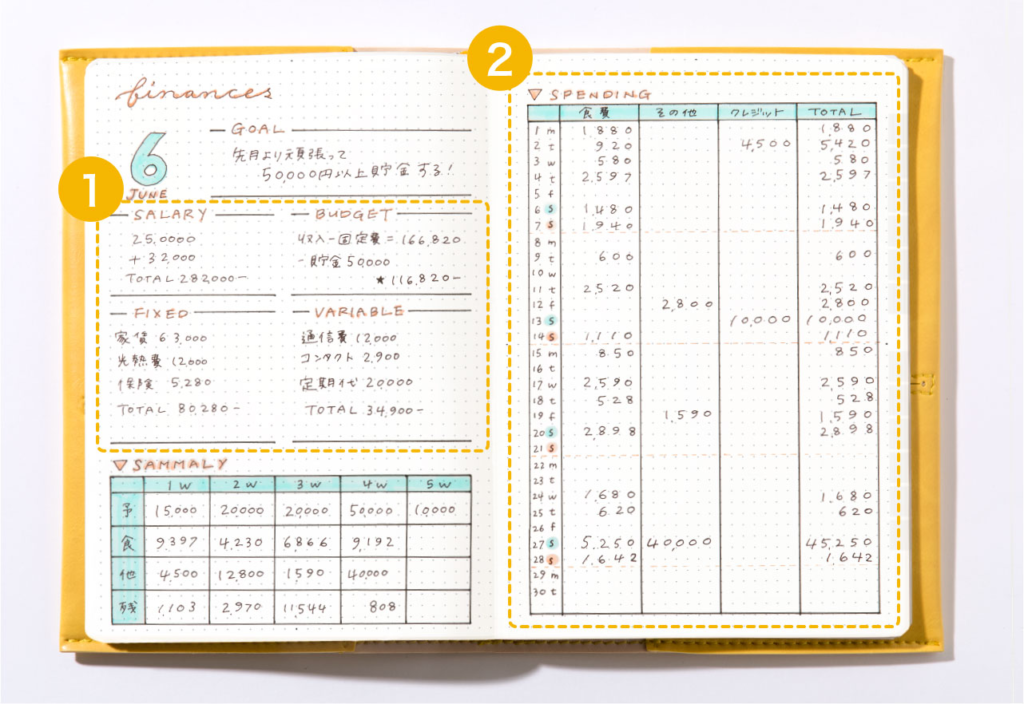

1. Kakeibo: The Spiritual Foundation of Saving

Before there were apps, there was Kakeibo (Household Account Book). This 120-year-old method of hand-writing every expense is the starting point for anyone wanting to save in Japan.

Many Western readers might be used to automated apps that track every cent. But in Japan, we still pick up the pen. It’s not because we lack the technology; it’s because we value the ‘pause’ that writing provides. While the West focuses on the efficiency of budgeting, Kakeibo focuses on the philosophy of it.

- The Power of the Pen: By physically writing down your spending, you face your habits. It’s not just accounting; it’s a daily meditation on your values.

2. Poikatsu: Navigating the Digital Ecosystem

In Japan, “Points” are more than just rewards; they are effectively a second currency. If you want to master the art of saving here, you must understand the “Big 5 Point Ecosystems”.

The Rise of QR Code Payments: Interestingly, many Japanese residents now prefer QR code payments (like PayPay) over traditional credit cards. Why? Because it aligns perfectly with the frugal mindset. QR payments provide instant visual feedback on your balance and spending—much like physical cash—making it easier to control your budget and see your points accumulate in real-time.

The Big 5 Points: Most Japanese consumers align their lifestyle with one of the major networks: Rakuten Point, d Point, PayPay Point, Ponta, and T-Point. By choosing specific convenience stores, supermarkets, or mobile carriers, you can maximize your returns daily.

Beyond Credit Cards: While credit card points are also used, Japan has traditionally been a cash-based society. This long-standing habit has shaped a unique preference in the digital age.

- Strategic Spending: From Rakuten to PayPay, residents meticulously choose where to shop based on point multipliers. It’s a game of efficiency that can save you thousands of yen every month.

3. Mottainai: Quality Living Through Second-Hand Markets

The concept of Mottainai (regret over waste) has created the world’s most high-quality second-hand market.

- Treasures in Used Goods: Platforms like Mercari and stores like Book-Off or 2nd Street allow you to live a premium life at a fraction of the cost. In Japan, “used” often looks brand new.

3. The Psychology of Cash: Why “Physical Money” Still Rules in Japan

While the rest of the world has rushed into a cashless future, Japan has remained a cash-based fortress for a long time. For a newcomer, carrying a heavy coin purse might feel like a hassle, but for many Japanese people, this “analog” habit is a deliberate strategy for financial discipline.

- The Weight of Spending: When you use a credit card, the transaction is invisible. But when you pay with cash, you physically feel the money leaving your hands. This creates a psychological “friction” that naturally makes you think twice before spending.

- Visualizing the Budget: Many practitioners of Kakeibo prefer using cash because of the immediate visual feedback. When you look into your wallet and see only a few 1,000-yen notes left, you don’t need an app to tell you that you’ve reached your limit for the week.

- The QR Hybrid Solution: This is why even as Japan moves toward digital payments, QR codes (like PayPay) have become more popular than credit cards. They act as a digital version of cash—you often “charge” them with a specific amount, and the app shows your remaining balance in big, bold numbers. It replicates that same feeling of a finite, visible budget.

My Insight: I used to find it strange to see people counting out coins at the register. But now, I realize they aren’t just paying; they are auditing their own lives. In a world of invisible digital debt, the Japanese “Cash-First” mindset is a powerful shield that keeps your feet—and your wallet—firmly on the ground.

4. Challenges: Inflation and the End of Cash-Is-King

However, this frugality superpower is now facing an unprecedented threat. For nearly 25 years, Japan lived in a deflationary society where prices never moved. In that world, simply “saving cash” was the smartest move you could make.

That era is over. Japan is now experiencing inflation that the current generation has never seen before.

- The Limits of Frugality: You can be the master of Kakeibo and Poikatsu, but you cannot “save” your way out of rising energy costs and a weakening Yen that erodes your purchasing power.

- From Saving to Investing: The myth that “cash in a bank account is safe” is breaking. Today, the conversation is shifting toward the importance of investment. While saving provides a shield, only strategic investment can provide the sword needed to protect your future in this new, inflationary Japan.

Conclusion: A New Mindset for a New Japan

Saving is still a virtue, and the tools like Kakeibo are more important than ever to build a foundation. But we must realize that the old myth is no longer enough. To thrive in Japan today, one must combine the traditional discipline of the past with the bold financial strategies of the future.

Leave a Reply